How to Calculate and Track Your Net Worth

Net worth is the single best number for tracking real financial progress, far better than income alone. Here's how to calculate it and track it over time.

Table of contents

If you've only ever tracked your income, you've been measuring the wrong number. Net worth tells a far more accurate story of real financial progress.

Short answer: Net worth is the total value of everything you own (assets) minus everything you owe (liabilities). Unlike income, it captures debt repayment, savings and investment growth in a single number, making it the clearest way to track genuine financial progress over time.

Why net worth matters more than income

Income tells you how much money passes through your hands. Net worth tells you how much of it you've actually kept and grown. Someone earning a high salary but carrying significant debt and no savings may have a lower net worth than someone earning less but saving and investing consistently.

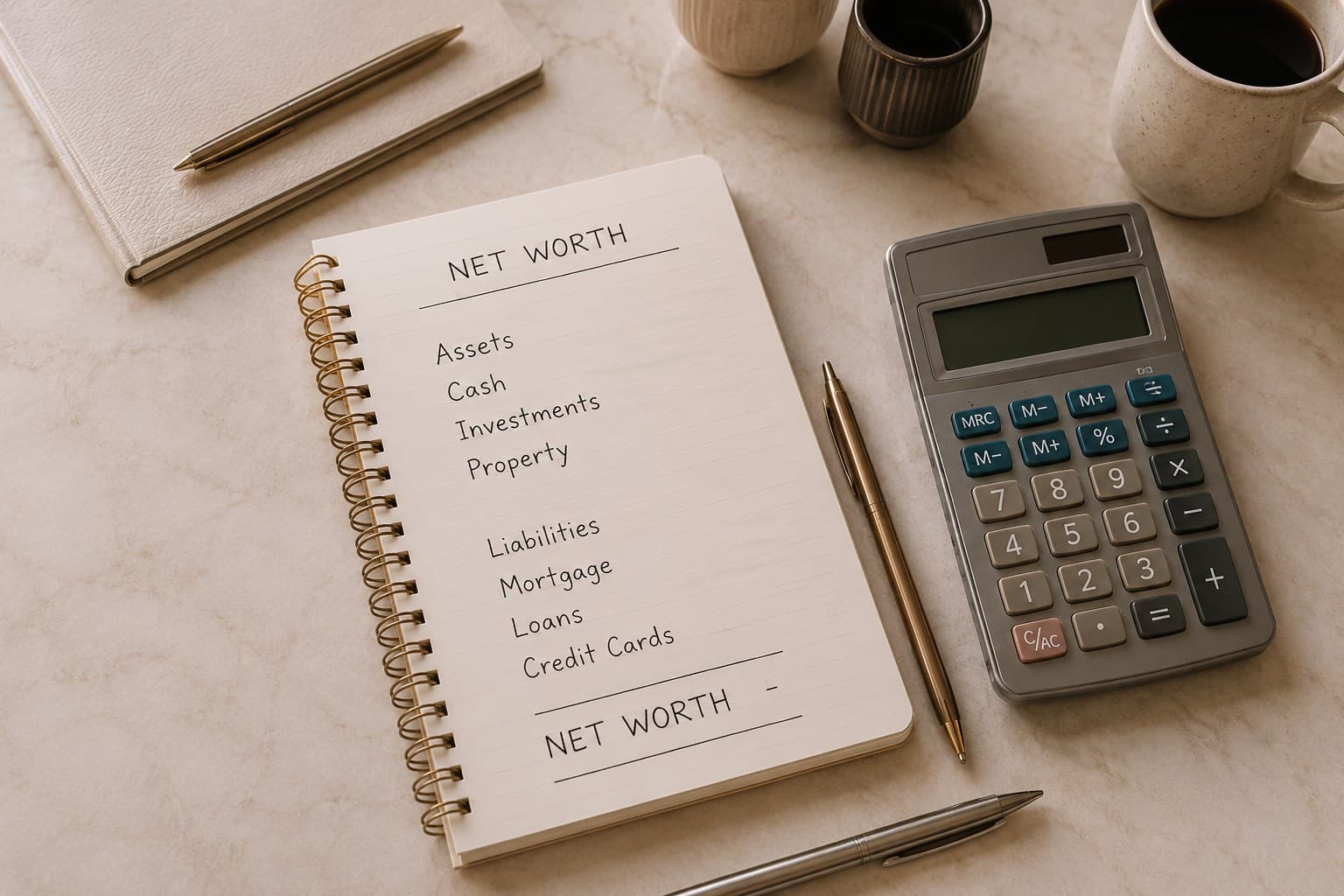

How to calculate your net worth

The formula is simple:

Net worth = Total assets − Total liabilities

Step 1: List your assets

- Cash in bank accounts

- Emergency fund and sinking funds

- Investments (stocks, funds, pensions)

- Property value (at current estimated market value)

- Any other valuable assets (vehicles, if significant)

Step 2: List your liabilities

- Mortgage balance

- Credit card balances

- Personal loans

- Student loans

- Any other outstanding debt

Step 3: Subtract liabilities from assets

Example

If your assets total £85,000 (savings, investments, and estimated home equity) and your liabilities total £60,000 (remaining mortgage and a small personal loan), your net worth is £25,000. That single number reflects debt repayment, saving and investing all at once.

A simple net worth tracking table

| Category | Example amount |

|---|---|

| Cash savings | £8,000 |

| Investments | £15,000 |

| Home value | £250,000 |

| Total assets | £273,000 |

| Mortgage balance | £230,000 |

| Credit card balance | £2,000 |

| Total liabilities | £232,000 |

| Net worth | £41,000 |

How often to track it

Every three to six months is usually the right rhythm, frequent enough to see meaningful trends, infrequent enough to avoid overreacting to short-term market swings that don't reflect real progress.

What actually matters: the trend, not the number

A single net worth snapshot means far less than its direction over time. A negative net worth (common with student loans or a new mortgage) isn't a failure if the trend line is steadily improving. Focus on the direction, not a single comparison point against someone else's number.

Common mistakes

| Mistake | Why it's misleading |

|---|---|

| Comparing your net worth to strangers online | Their income, location and life stage are rarely comparable to yours. |

| Checking it too frequently | Daily market movements create noise that obscures real long-term progress. |

| Excluding debt from the calculation | Net worth without liabilities isn't net worth, it's just a partial asset list. |

| Panicking over a single bad quarter | Short-term dips are normal; the multi-year trend is what matters. |

Key takeaways

- Net worth (assets minus liabilities) is a far more accurate measure of financial progress than income alone.

- Track it every three to six months to see meaningful trends without overreacting to short-term noise.

- The trend over time matters more than any single snapshot or comparison to others.

- Include both assets and debts for an honest, complete picture.

Understanding your numbers is powerful, but money doesn't exist in a vacuum. The next step is looking at how everyday life decisions, from careers to relationships, shape your finances too.

The Personal Finance Guide

The complete, step-by-step system for understanding your money.

A calm, step-by-step walkthrough of exactly how to organise your money — from your first budget to your first investment, explained simply and without the jargon.

Frequently asked questions

Ana

Founder, Understand Money with Ana

I spent most of my 20s avoiding my bank balance. Understand Money with Ana breaks down budgeting, saving and investing in plain English — the way I'd explain it to my own sister.

More about Ana →Related articles

What Financial Independence Actually Means (And How to Get There)

Financial independence isn't one magic number or an early retirement fantasy. Here's what it actually means, and a realistic path toward it.

FIRE Explained: What It Means to Retire Early

FIRE stands for Financial Independence, Retire Early, but it's not one single approach. Here's what it actually means, and the main variations within the movement.

The Complete Emergency Fund Guide: How Much to Save and Where to Keep It

How much should your emergency fund actually be, and where should you keep it? A clear, step-by-step guide to building your financial safety net.