Sinking Funds Explained: The Saving Strategy That Stops Surprise Expenses

Sinking funds are the simplest way to stop 'unexpected' expenses from wrecking your budget. Here's exactly what they are and how to set them up.

If a "surprise" car insurance renewal or annual subscription always seems to catch you off guard, the fix isn't better willpower, it's a sinking fund.

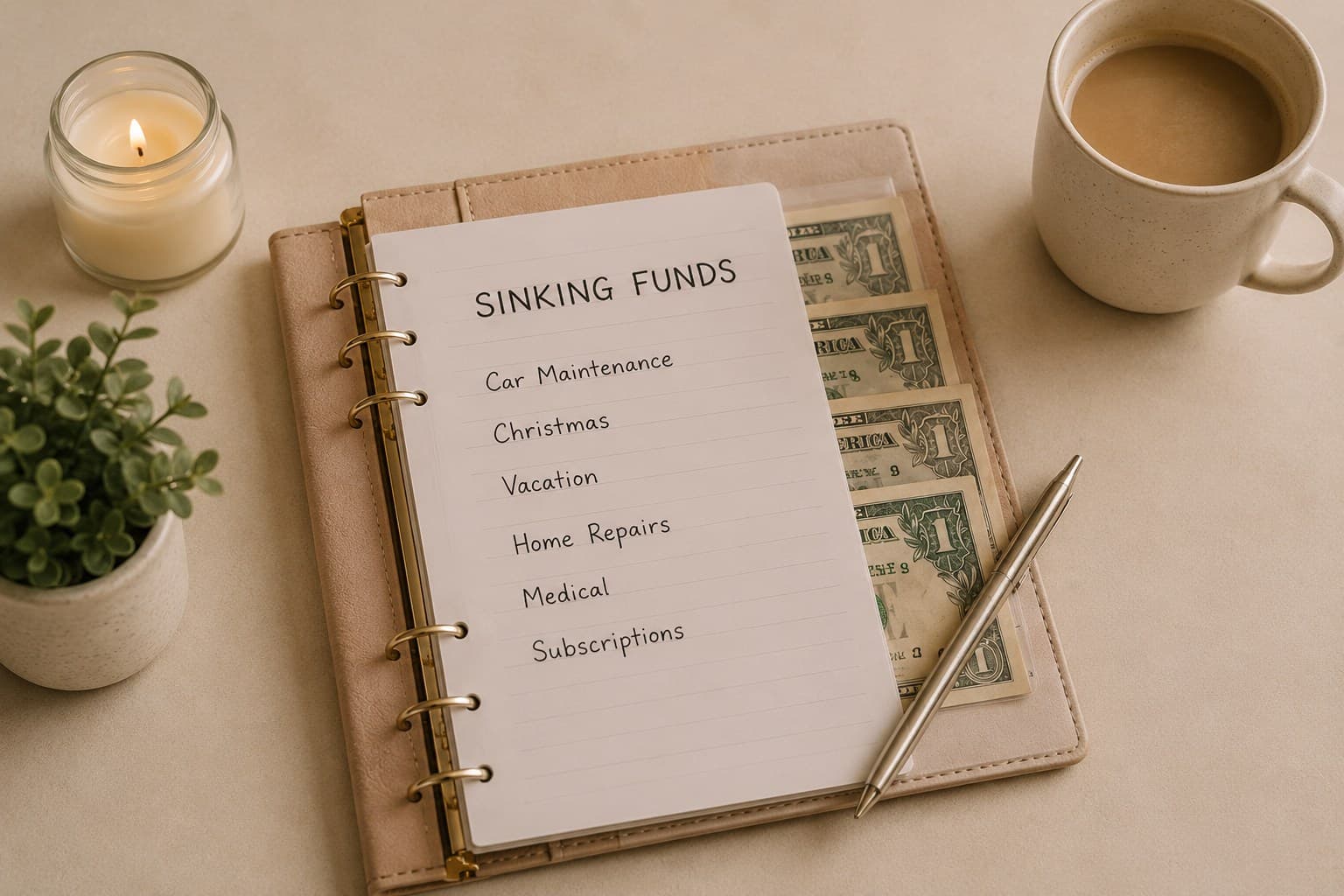

Short answer: A sinking fund is money you save gradually, ahead of time, for a specific expense you know is coming, like a holiday, car maintenance, or an annual renewal, so it never has to be paid for out of a single month's budget all at once.

What makes a sinking fund different from an emergency fund

It's easy to confuse the two, but the distinction matters:

- Emergency fund, for the unpredictable: job loss, medical bills, a burst pipe.

- Sinking fund, for the predictable: you know it's coming, you just don't want it to hit one month all at once.

Car insurance renewing every 12 months isn't an emergency, you know it's coming. Treating it as one is exactly what makes it feel like a nasty surprise every single year.

How to set one up

- List your irregular but predictable expenses. Common ones: car insurance, car maintenance, annual subscriptions, holidays, gifts, home maintenance, back-to-school costs.

- Estimate the annual cost of each. Even a rough estimate is enough to start.

- Divide by 12. That's your monthly contribution for that specific fund.

- Automate a transfer into a dedicated savings account (or clearly labelled pot within one) each month.

Example

If your car insurance renews at £600 a year, saving £50 a month means the renewal is already covered when it arrives, instead of appearing as a painful £600 hit to a single month's budget.

A simple sinking fund table

| Sinking fund | Estimated annual cost | Monthly contribution |

|---|---|---|

| Car insurance | £600 | £50 |

| Car maintenance | £480 | £40 |

| Holiday | £1,200 | £100 |

| Gifts (birthdays, holidays) | £360 | £30 |

Adjust the categories and amounts to match your own life, the structure matters more than the exact numbers.

Where to keep sinking funds

Most banking apps now offer "pots" or "spaces" that let you separate sinking funds within one account, which works well and keeps things simple. If your bank doesn't offer this, a dedicated savings account with a clear label works just as well.

Common mistakes

- Lumping everything into one general savings account. Without separation, it becomes unclear how much is actually "safe" to spend versus earmarked for something specific.

- Only using sinking funds for large annual costs. Smaller, more frequent irregular costs (like gifts) benefit just as much.

- Forgetting to adjust amounts year to year. Costs like insurance rise, revisit your estimates annually.

Key takeaways

- Sinking funds are for predictable expenses; emergency funds are for unpredictable ones.

- Divide the annual cost of a recurring expense by 12 to find your monthly saving target.

- Automating the transfer removes the need to remember or rely on willpower.

- Review and adjust your sinking fund amounts once a year as costs change.

Once your saving system is running smoothly, the next question is simple: is your money actually earning what it should be? That's where high-yield savings accounts come in.

The Personal Finance Guide

The complete, step-by-step system for understanding your money.

A calm, step-by-step walkthrough of exactly how to organise your money — from your first budget to your first investment, explained simply and without the jargon.

Frequently asked questions

Ana

Founder, Understand Money with Ana

I spent most of my 20s avoiding my bank balance. Understand Money with Ana breaks down budgeting, saving and investing in plain English — the way I'd explain it to my own sister.

More about Ana →Related articles

The Complete Emergency Fund Guide: How Much to Save and Where to Keep It

How much should your emergency fund actually be, and where should you keep it? A clear, step-by-step guide to building your financial safety net.

High-Yield Savings Accounts Explained (And Why Yours Might Be Costing You)

If your savings are sitting in a standard account earning almost nothing, you could be quietly losing money to inflation. Here's what a high-yield savings account is and how to choose one.

How to Create a Budget You'll Actually Stick To

Most budgets fail within a month because they're too restrictive to survive real life. Here's how to build a simple, flexible budget you'll actually keep using.